Can I Withdraw Super: Everything You Need to Know

Introduction

Superannuation, also known as “super,” is a key concept in Australia when it comes to retirement planning and savings. It acts as a tax-efficient way to save money for retirement. Although super is meant for long-term investments, there are times when people may encounter situations that require them to access these money prior to retirement. We will examine the qualifying requirements, potential repercussions, and other solutions to take into account in this extensive guide.

Understanding Superannuation

1.1 What is Superannuation?

In Australia, the term “superannuation” refers to the legally required retirement savings program. Employers make contributions on behalf of their employees, and individuals also make additional voluntary contributions. As you can withdraw super, these funds are then invested in a variety of assets to increase over time, ensuring financial stability during retirement.

1.2 How Does Superannuation Work?

Your employer must start paying mandatory contributions to your super fund as soon as you start working. Additionally, you have the option to salary sacrifice additional contributions from your pre-tax or post-tax income. Your super fund’s collected funds are invested to produce returns in a varied portfolio of securities, including equities, bonds, and real estate.

1.3 Importance of Superannuation for Retirement

Your ability to secure your financial future after retirement depends heavily on superannuation. You can maintain a decent lifestyle and reduce your dependency on government pensions thanks to the regular income stream provided by super once you turn 65. You are also eligible to withdraw from super.

The Early Withdrawal Option

2.1 Eligibility for Early Withdraw super.

Superannuation is typically protected until you reach your preservation age, which varies depending on your birth year but is often between 55 and 60, and satisfy a condition of release, such as retirement or turning 65. However, there are some circumstances in which early withdrawal might be permitted.

2.2 Conditions of Release

Severe financial hardship, compassionate grounds, terminal sickness, and permanent incapacity are some frequent situations that may permit an early super withdrawal. To be eligible for early access, a precise set of requirements for each condition must be satisfied.

2.3 Pros and Cons of Withdraw Super Early

While early access to super can offer temporary comfort during trying times, it’s crucial to take the long-term impact into account. Early withdrawals can lower your retirement funds, which may have an impact on your future financial security.

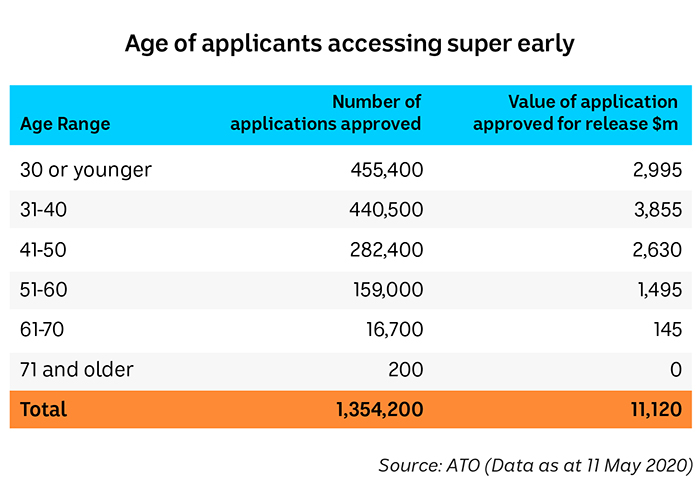

COVID-19 Related Withdrawals

3.1 How the Pandemic Affected withdraw Super Withdrawals

Many people experienced unheard-of financial troubles as a result of the COVID-19 outbreak. The Australian government gave those negatively impacted by the epidemic temporary early access to super to lessen some of the responsibilities.

3.2 Special Provisions during COVID-19

Eligible persons were allowed to withdraw up to $10,000 during the epidemic in the 2019–2020 fiscal year and another $10,000 during the 2020–2021/21 fiscal year. This short-term initiative aims to give individuals in serious financial need quick assistance.

Withdrawing Super for First Home Buyers

4.1 The First Home Super Saver Scheme

The First Home Super Saver (FHSS) Scheme is a government program created to help first-time homebuyers save for a down payment on a house using their superannuation.

4.2 Eligibility and Withdrawal Process

You must meet specific requirements, such as never having owned property in Australia previously, in order to be eligible for the FHSS Scheme. Those who qualify may request the release of voluntary contributions they made to their retirement accounts for the purpose of getting their first home.

4.3 Impact on Retirement Savings

While the FHSS Scheme presents a special opportunity for first-time homebuyers, it’s important to understand that taking money out of super for this use decreases the amount of money you’ll have for retirement.

Financial Hardship and Compassionate Grounds

5.1 Qualifying for Financial Hardship

You might be able to receive a portion of your superannuation early in circumstances of extreme financial difficulty to relieve the pressure on your current finances.

5.2 Compassionate Grounds Eligibility

Withdrawals on compassionate grounds are allowed in certain situations, such as for the cost of medical care, palliative care, or funeral expenditures.

5.3 Withdrawal Limits and Tax Considerations

There are restrictions on how much you can withdraw for compassionate or economic reasons. You should also be aware of any potential tax repercussions associated with these withdrawals.

Taxation on Super Withdrawals

6.1 Tax on Preserved and Unpreserved Amounts

Depending on whether the funds are maintained or not, super withdrawals are subject to various tax treatments.

6.2 Impact on Government Benefits

Your eligibility for government benefits like the Age Pension may be impacted by super withdrawals. In order to make wise judgements, it is essential to understand the potential effects.

Alternatives to Withdrawing Super

7.1 Personal Savings and Emergency Funds

Investigate using personal savings or emergency funds to manage financial issues before thinking about early super withdrawals.

7.2 Other Investment Options

Investigating non-traditional investing possibilities might improve financial results without jeopardizing long-term retirement plans.

Seeking Professional Advice

8.1 Consulting a Financial Advisor

It can be difficult to navigate the complications of early withdrawals and superannuation. You can get clarity and make well-informed decisions for your financial future by seeking the assistance of a knowledgeable financial advisor.

Planning for Retirement: Tips for a Secure Future

9.1 Understanding Your Retirement Needs

Spend some time evaluating your financial needs and retirement needs while taking into account aspects of your way of life, your health, and your leisure pursuits.

9.2 Making Additional Contributions

To increase your superannuation funds and hasten the process of reaching a secure retirement, think about making additional voluntary contributions.

9.3 Diversifying Your Investments

In order to manage risk in your investing portfolio, diversification is essential. To achieve balanced and sustainable development, think about diversifying your super investments.

9.4 Reviewing Your Super Regularly

Financial objectives change as do life situations. Maintaining alignment with your changing requirements and objectives requires routinely assessing your superannuation approach.

Conclusion

A great tool for ensuring your financial security in retirement is superannuation. Although there are opportunities for early withdrawal under certain circumstances, the repercussions must be carefully considered. It’s critical to balance the demand for quick cash with any potential effects on long-term retirement savings. You can navigate these options successfully by seeking professional counsel and looking into different financial options.

FAQs

1. Can I withdraw my super for a holiday or luxury purchase?

No, it is not legal in Australia to withdraw super for things like vacations or opulent purchases that are not eligible.

2. Will withdrawing super early affect my insurance coverage within the super fund?

Yes, using your super early may have an effect on your insurance coverage, possibly resulting in policy cancellations or coverage cutbacks.

3. Is there a limit on how many times I can withdraw my super early?

Specific circumstances for early super withdrawal can only be used when eligibility requirements are satisfied.

4. Can I access my spouse’s super if I am facing financial hardship?

No, even in times of dire straits you cannot access your spouse’s superannuation funds.